2025-11-12

Six tips to spend smarter this summer

Bankruptcy Consumer Proposal

Summer fun doesn’t have to come with a hefty price tag.

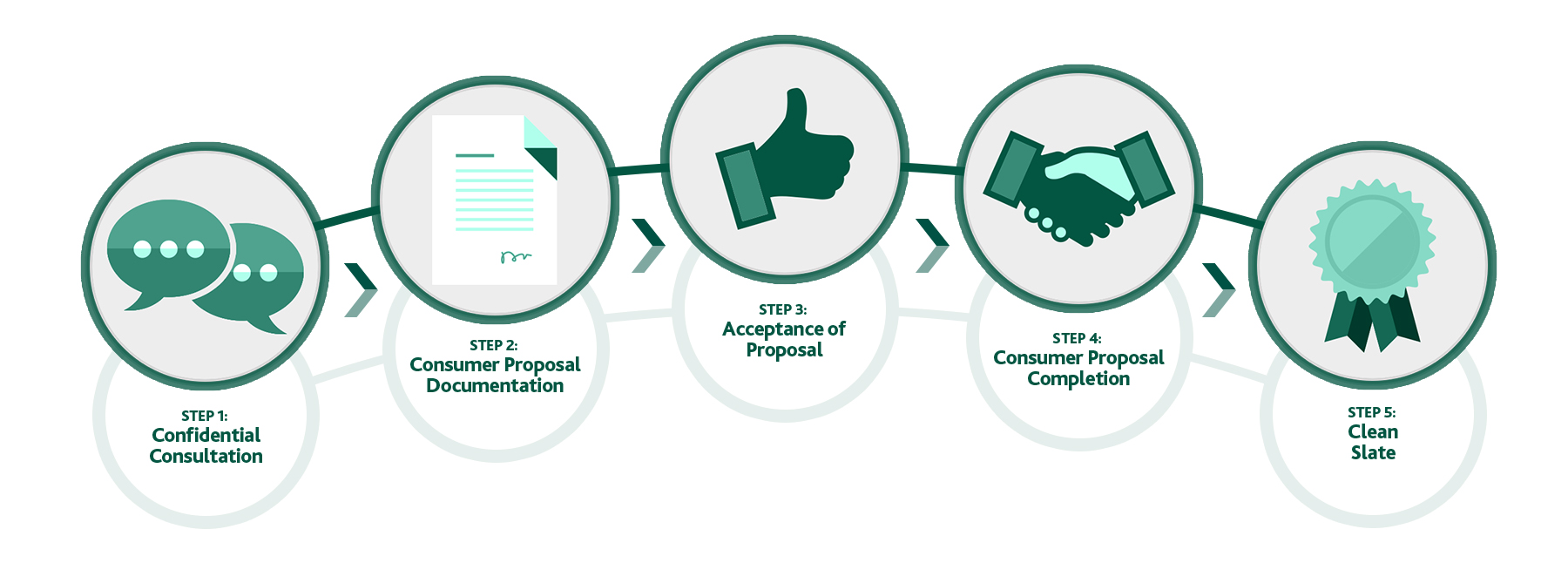

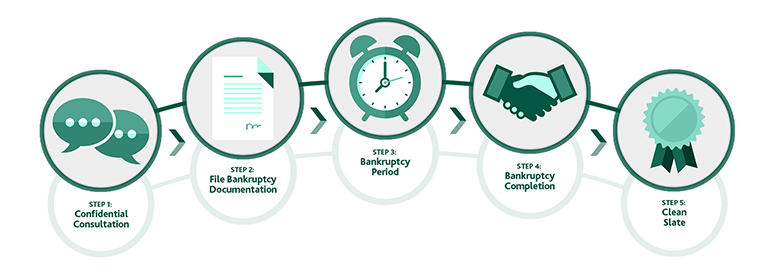

Consumer Proposals and bankruptcies are both government legislated options which can provide you with relief from significant debt problems. In addition, both debt solutions can only be administered by a Licensed Insolvency Trustee and provide a legal stay of proceedings which require creditors to discontinue harassing collection calls, garnishment or other legal proceedings.

Determining which, if either, option is an appropriate solution in your own unique situation depends on a number of variables. Let’s explore the advantages and disadvantages of both a Consumer Proposal and a bankruptcy.

2025-11-12

Bankruptcy Consumer Proposal

Summer fun doesn’t have to come with a hefty price tag.

2025-11-07

Bankruptcy Consumer Proposal

If you're facing a mountain of debt, you're not alone. There are two viable options available to help you find relief: Consumer Proposal and Bankruptcy. Each approach offers unique benefits that can be tailored to fit your specific financial situation.

2025-10-20

Alternatives to Bankruptcy Bankruptcy Consumer Proposal Lifestyle Debt MNP Consumer Debt Index

Just when seniors should be relaxing and enjoying the fruits of their labour, many find themselves struggling financially — an unsettling contrast to the ease they’d hoped to live their golden years.