Debt Literacy Month: Nearly half of Canadians regret their debt as persistent debt blind spots leave many financially vulnerable

2026-03-02

schedule6 minute read

Author:

Grant Bazian

Five years of national data show financial resilience remains constrained, with debt literacy challenges leaving many Canadians vulnerable to financial shocks and the long-term impact of borrowing costs.

CALGARY, AB – March 2, 2026 – Five years of national tracking data, compiled by Ipsos on behalf of MNP LTD, show that debt concern remains elevated among Canadians, financial preparedness has declined, and debt literacy lags as financial pressures persist.

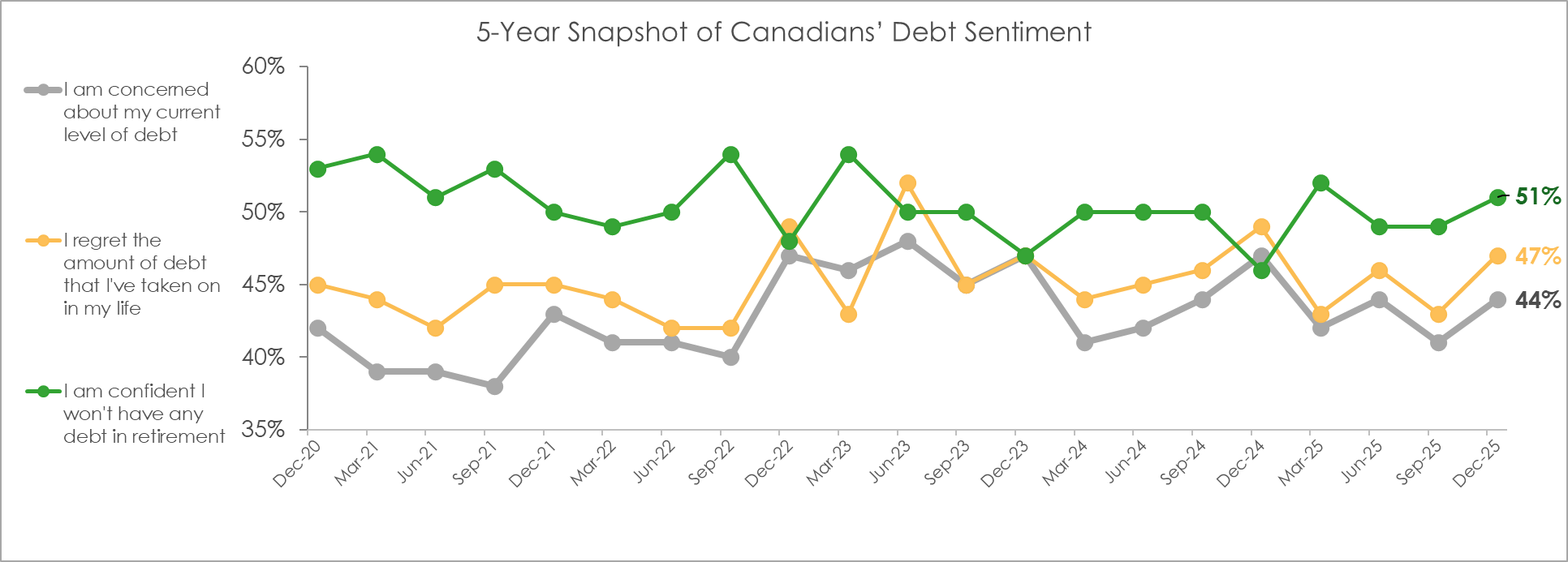

More than two in five Canadians (44%, +2 pts vs. 2020) say they are concerned about their current level of debt. Nearly half (47%, +2 pts vs. 2020) regret the amount of debt they have taken on. Only half of Canadians (51%, -2 pts vs. 2020) believe they will be debt-free in retirement. Debt anxiety is especially pronounced among younger generations. Concern about current debt is highest among Gen Z (55%, +13 pts vs. 2020) and Millennials (55%, unchanged vs. 2020). Three in five Millennials (59%, +2 pts vs. 2020) say they regret the amount of debt they have taken on, the highest proportion of any age group.

Source: Ipsos on behalf of MNP LTD

Caption: From 2022 onward, measures of debt concern, debt regret, and confidence in being debt-free in retirement show greater quarter-to-quarter variation among Canadians, consistent with a period of economic adjustment. In 2024 and 2025, the three measures move within a narrower range than in prior years, suggesting less separation between Canadians’ views of their past, present, and future debt.

While borrowing has become more common amid cost-of-living pressures, many Canadians remain unclear on how interest works in practice and how rate changes affect their financial position. One in five Canadians (20%, -5 pts vs. 2020) say they do not have a solid understanding of how interest rate increases impact their financial situation. This indicates that while there has been modest improvement over five years, significant knowledge gaps remain.

“The data underscores the need for stronger debt literacy across the country. It is not enough to be aware of balances owed. A practical understanding of compounding interest, rate sensitivity, and contingency planning is increasingly important in today’s environment,” says Grant Bazian, president of MNP LTD, the country’s largest insolvency firm. “The compounding effect of interest can carry significant long-term consequences. Over a five-year period, for example, debt can behave like financial quicksand as borrowing costs compound quietly, and even small interest rate increases can deepen the burden over time. What begins as manageable can gradually extend repayment timelines and inflate total interest paid.”

MNP is marking Debt Literacy Month this March with a focus on debt blind spots, helping Canadians better understand where their financial vulnerabilities exist, how quickly circumstances can change, and why planning for unexpected life events matters.

“Financial shocks often push people into debt or deepen existing debt. Debt literacy is what helps Canadians recognize the warning signs early, understand the trade-offs of relying on credit, and know their options before a situation escalates,” says Bazian.

Canadians report feeling less equipped to handle unexpected life events compared to five years ago, as unresolved debt blind spots leave households more vulnerable when unexpected income loss or expenses occur. The most recent data shows that Canadians recorded negative confidence scores for every unexpected life event tested — and those scores have all worsened since 2020. This underscores that many of the same risk-readiness blind spots persist today.

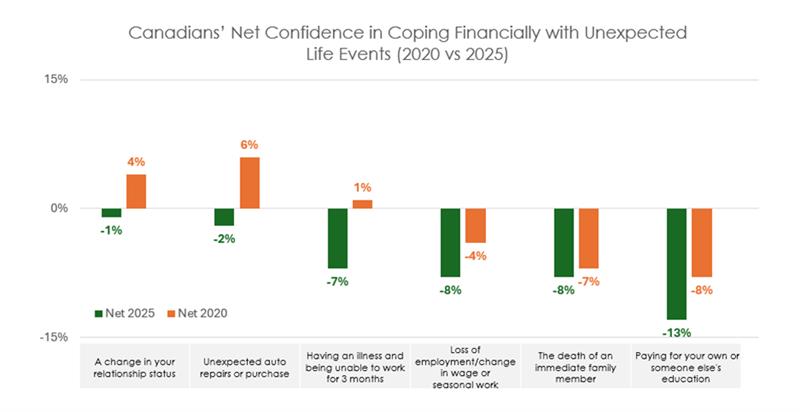

Source: Ipsos on behalf of MNP LTD

Caption: In a side-by-side comparison of 2020 and 2025, Canadians’ net confidence in coping financially with unexpected life events is lower across all categories, and all measures now fall in negative territory.

Unexpected financial shocks such as education costs (-13%, -5 pts vs. 2020), job loss (-8%, -4 pts vs. 2020), the death of an immediate family member (-8%, -1 pt vs. 2020), and an illness preventing work for at least three months (-7%, -8 pts vs. 2020) showed the greatest vulnerability. Relationship changes such as divorce or separation (-1%, -5 pts vs. 2020) and unexpected auto repairs or vehicle purchase (-2%, -8 pts vs. 2020) also remained in negative territory.

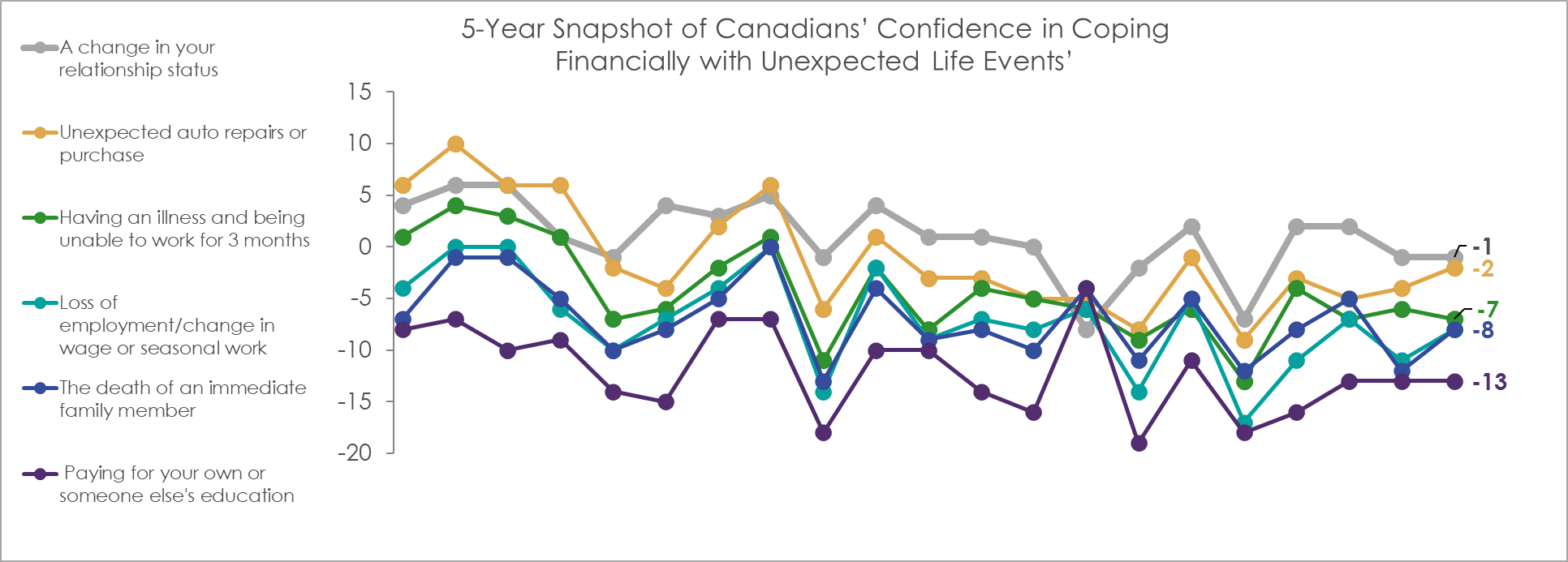

Source: Ipsos on behalf of MNP LTD

Caption: Starting in 2022, Canadians’ confidence in handling unexpected life events exhibits greater quarter-to-quarter fluctuation, reflecting a period of economic adjustment. In 2024 and2025, the measures remain firmly in negative territory, underscoring that many Canadians report low confidence in their ability to cope with major financial shocks.

Taken together, the findings suggest that while Canadians recognize these risks, many have low confidence in their ability to absorb them in practice, particularly in today’s higher-cost environment.

“Sudden changes in circumstances can strain household finances quickly, particularly for individuals who are already relying on credit to manage everyday expenses,” says Bazian. “The most common triggers that push people into unmanageable debt are relationship breakdowns and job loss or reduced income. Seeking qualified advice early can help individuals understand their options and make informed decisions before financial pressures increase.”

Gaps in debt literacy, such as how interest rate increases impact personal finances, can compound financial risk over time. This can make it harder to stay prepared for unexpected life events. When people underestimate how quickly interest adds to their balances, a sudden life shock can turn manageable debt into something more difficult to handle.

“Misunderstanding interest can lead people to underestimate how quickly balances grow, rely too heavily on minimum payments, or delay seeking debt help until their situation becomes difficult to manage,” says Bazian. “Making only minimum payments can mean carrying debt for decades and paying several times the original purchase price in interest. As compounding interest builds over time, it’s easy to misjudge how serious the situation is becoming. That’s why having access to clear, impartial guidance about their financial situation is so important.”

Closing debt blind spots and finding the right support

- Calculate the true cost of your debt, not just the balance.

Do not focus only on what you owe today. Use an amortization calculator to determine how much interest you will pay over time, especially if you are making only minimum payments.

- Stop relying on minimum payments as a strategy.

Minimum payments often extend repayment for years or even decades. Paying more than the minimum whenever possible helps reduce the long-term impact of compounding interest.

- Build a financial buffer.

Start with a goal of one month of essential expenses. Even small emergency savings can reduce reliance on high-interest credit during unexpected events.

- Review your repayment timelines, interest rate type, and exposure.

Revisit your debt plan each year to ensure you remain on track and are not drifting further from repayment due to compounding interest. Know which debts are variable, fixed, promotional, or nearing the end of an introductory period. Blind spots often arise when low rates expire.

- Use free assessment tools to benchmark your situation.

If you are hesitant to seek in-person advice, start with objective tools to evaluate whether your current repayment path is sustainable. Free online Do-It-Yourself debt assessment tools allow users to better understand their situation.

- Separate lifestyle normalization from financial reality.

Borrowing may feel common, but that does not make it low risk. Normalize reviewing your debt regularly rather than carrying it indefinitely.

- Create a written ‘what if’ plan.

Outline how you would respond to job loss, illness, or a major expense. Having a plan in place reduces reactionary borrowing decisions.

- Seek guidance from a Licensed Insolvency Trustee.

Licensed Insolvency Trustees are the only federally regulated professionals in Canada who can assist with all the debt relief options, including Consumer Proposals and Bankruptcy, stop harassment from debt collectors, and discharge people from debt. In many cases, they help indebted individuals explore alternatives to Bankruptcy and regain financial stability. This often includes clarifying how interest compounds over time, how minimum payments affect overall balances, and realistic timelines for becoming debt-free.

- Do not wait until the situation feels urgent.

Many people delay seeking help until financial pressure feels overwhelming. Speaking with a Licensed Insolvency Trustee early typically means more available options and greater flexibility. Life shocks such as job loss, illness, or relationship changes can occur without warning. Having a conversation with a Licensed Insolvency Trustee sooner can help prevent a temporary setback from becoming a long-term financial crisis.

“Speaking with a Licensed Insolvency Trustee is often the best first step for anyone feeling overwhelmed by debt,” says Bazian. “We take a holistic look at each person’s situation, help them understand what’s realistically achievable, and create a clear, practical plan that puts them back in control of their finances.”

MNP’s national team of Licensed Insolvency Trustees offers free consultations across the country to help severely indebted Canadians get unbiased debt advice, understand their rights, and determine the best path forward.

About MNP LTD

MNP LTD, a division of the national accounting firm MNP LLP, is the largest insolvency practice in Canada. For more than 50 years, our experienced team of Licensed Insolvency Trustees and advisors have been working with individuals to help them recover from times of financial distress and regain control of their finances. With more than 240 offices from coast to coast, MNP helps thousands of Canadians each year who are struggling with an overwhelming amount of debt. Visit MNPdebt.ca to contact a Licensed Insolvency Trustee or use our free Do-it-Yourself (DIY) debt assessment tools. For regular, bite-sized insights about debt and personal finances, subscribe to the MNP 3-Minute Debt Break Podcast.

About the Survey

Now in its thirty-fifth wave, this tracking, which has been conducted since 2017, measures Canadians’ attitudes toward their consumer debt, confidence in managing household finances, and aspects of their debt literacy. The survey provides evidence-based insights that support broader efforts to improve debt literacy. This includes identifying gaps in understanding, determining where financial vulnerabilities may exist, and helping Canadians better understand and manage their household debt.

The data was compiled by Ipsos on behalf of MNP LTD between November 28 and December 1, 2025. For this survey, a sample of 2,001 Canadians aged 18 years and over was interviewed. Weighting was then employed to balance demographics to ensure that the sample's composition reflects that of the adult population according to Census data and to provide results intended to approximate the sample universe. The precision of Ipsos online polls is measured using a credibility interval. In this case, the poll is accurate to within ±2.7 percentage points, 19 times out of 20, had all Canadian adults been polled. The credibility interval will be wider among subsets of the population. All sample surveys and polls may be subject to other sources of error, including, but not limited to, coverage error and measurement error.

Latest Blog Posts

2026-07-13

Tina Powell

MNP Consumer Debt Index

Atlantic Canadians (68%) are more likely than those in other provinces to say at least half of their income is already committed to bills, debt payments, and regular expenses before it arrives.

Read More

arrow_forward

2026-07-13

Grant Bazian

MNP Consumer Debt Index

According to the latest MNP Consumer Debt Index, three in five Canadians (61%) say at least half of their income is already committed to bills, debt payments, and regular expenses before it arrives.

Read More

arrow_forward

2026-07-13

Linda Paul

MNP Consumer Debt Index

According to the latest MNP Consumer Debt Index, nearly three in five British Columbians (58%) say at least half of their income is already committed to bills, debt payments, and regular expenses before it arrives.

Read More

arrow_forward