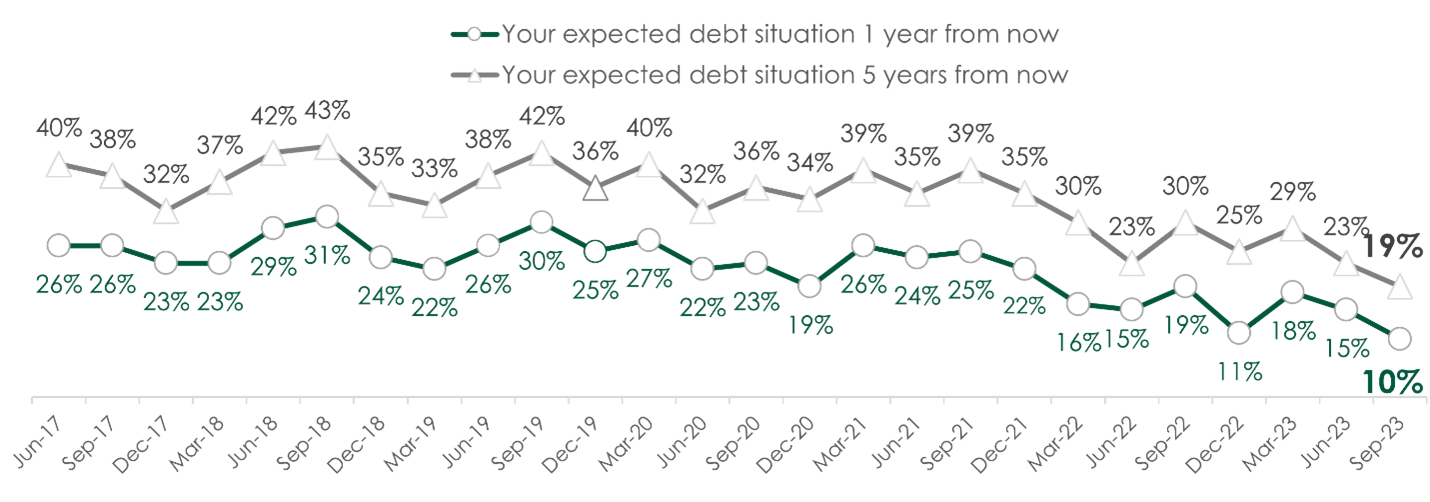

CALGARY, AB – October 18, 2023 – From near zero to the highest interest rates in more than two decades, the latest MNP Consumer Debt Index reveals that Canadians’ debt outlook has reached the most pessimistic point since tracking began five years ago. Reflecting on their current debt situation, more households rate their current situation as much worse than it was one (20%, +2) and five years ago (25%, +3) compared to the previous quarter (20%). Looking into the future, more believe their debt situation will worsen over the next year (18%, +3) and five years from now (16%, +2). Fewer also see any potential for improvement over the next five years (35%, -2).

Expected debt has been steadily declining since March 2021, with the COVID-19 pandemic and has reached the lowest recorded points. Looking forward to 1 year from now, Canadians' net score (much better [8-10] minus much worse [1-3]) on their debt situation dropped to 19% and looking five years from now dropped to 10%.

“There is no mystery as to what is causing Canadians’ bleak debt outlook. It’s getting more difficult to make ends meet,” says Grant Bazian, President of MNP LTD, the country’s largest insolvency firm. “Facing a combination of rising debt carrying costs, living expenses and concern over the potential for continued interest rate and price hikes, many households are stretched uncomfortably close to broke.”

More than half (51%, -1) of Canadians report that they are $200 away or less from not being able to meet all their financial obligations. That includes three in 10 (31%, -4) who already don’t earn enough to cover their bills and debt payments. The average amount Canadians say they have left over at the end of the month dropped to $674 (-$97) as the surging cost of living has chipped away at household budgets.

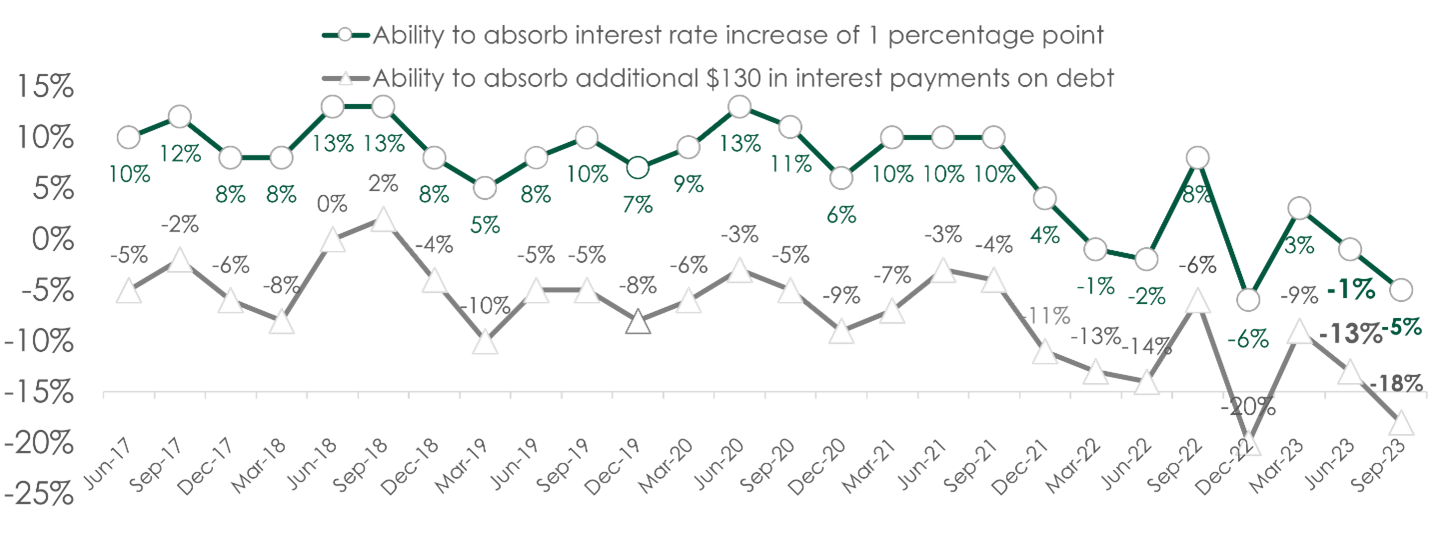

When it comes to the potential for future interest rate increases, Canadians feel worse about their ability to absorb further hikes compared to last quarter. A quarter (28%, +5) say their ability to deal with an increase of one percentage point has worsened. When this question was rephrased to ask their ability to absorb an interest rate increase of an extra $130, four in 10 (37%, +5) say their ability to absorb this increase is much worse, and a fifth (19%, unchanged) say it is much better.

Canadians are feeling worse about their ability to absorb interest rate hikes. When asked about their ability to absorb an interest rate increase of one percentage point or $130 in interest payments on debt, net scores have declined for three consecutive quarters, reaching the second lowest point since tracking began five years ago.

While Canadians’ debt outlook and ability to absorb additional interest rates have deteriorated, there were a few bright spots in the data. Overall, the MNP Consumer Debt Index improved slightly to 86 points, up three points since last quarter. Still, it remains below the five-year average.

As for what’s driving the increase, Canadians are feeling marginally better about the possibility that rising interest rates will impact their ability to repay their debts (62%, -4), force them into financial trouble (60%, -3), or drive them towards Bankruptcy (45%, -5). Perhaps signalling that households are adjusting to the new normal of a higher interest rate environment, far fewer regret the amount of debt they’ve taken on (45%, -7 pts). Moreover, fewer are concerned about their current level of debt (45%, -3) or worried about someone in their household potentially losing their job (38%, -2).

“For now, the strong job market appears to have offset the financial concerns of some Canadians, at least to a degree. The uncomfortable truth is that higher interest rates should cool down the economy. That inevitably comes with consequences like increased unemployment,” says Bazian.

He says that higher unemployment and underemployment — where individuals either don’t earn enough or receive enough hours to cover their household expenses — is one of the leading causes of insolvency.

“Bills, debt obligations, and the ever-increasing cost of living may be somewhat manageable provided income remains consistent. Those costs can quickly become troublesome if the unexpected occurs, especially because many households have already cut back on non-essential spending,” he says.

“That’s when the danger of relying on credit to meet basic household needs becomes a real risk. Households initially use credit with the idea that the reduced income is temporary and that they can pay off the debt as soon as their circumstances improve. But as the bills mount, more of them go onto credit. Then, they start to make minimum payments. Then, they start to miss payments. And that’s how people end up on a high-interest debt treadmill,” he explains.

The consequences of missed payments, compounding interest, repossessions, or foreclosures can be swift and have long-lasting effects. Bazian recommends those who anticipate missing payments first contact their lender to see if they can set up a payment plan, then seek advice from a Licensed Insolvency Trustee.

“In addition to contacting their lenders, we advise anyone facing the challenge of escalating debts to speak with a Licensed Insolvency Trustee for a confidential financial assessment. A trustee can provide free and impartial advice on various debt relief solutions, including budgeting, debt consolidation, Consumer Proposals, and Personal Bankruptcy."

Licensed Insolvency Trustees are the only federally regulated debt professionals who can assist with all the debt relief options — including Consumer Proposals and Bankruptcy, which can immediately stop harassment from debt collectors — and discharge people from debt. To support those in need of financial assistance, MNP provides free consultations across the country.

About MNP LTD

MNP LTD, a division of the national accounting firm MNP LLP, is the largest insolvency practice in Canada. For more than 50 years, our experienced team of Licensed Insolvency Trustees and advisors have been working with individuals to help them recover from financial distress and regain control of their finances. With more than 240 offices from coast to coast, MNP helps thousands of Canadians each year who are struggling with an overwhelming amount of debt. Visit MNPdebt.ca to contact a Licensed Insolvency Trustee or use our free Do it Yourself (DIY) debt assessment tools. For regular, bite-sized insights about debt and personal finances, subscribe to the MNP 3-Minute Debt Break Podcast.

About the MNP Consumer Debt Index

The MNP Consumer Debt Index measures Canadians’ attitudes toward their consumer debt and gauges their ability to pay their bills, endure unexpected expenses, and absorb interest-rate fluctuations without approaching insolvency. Conducted by Ipsos and updated quarterly, the Index is an industry-leading barometer of financial pressure or relief among Canadians.

Now in its twenty-sixth wave, the Index increased to 86 points, up three points since last quarter, but remains below the five-year average. Visit MNPdebt.ca/CDI to learn more.

The data was compiled by Ipsos on behalf of MNP LTD between September 5 and September 8, 2023. For this survey, a sample of 2,000 Canadians aged 18 years and over was interviewed. Weighting was then employed to balance demographics to ensure that the sample's composition reflects that of the adult population according to Census data and to provide results intended to approximate the sample universe. The precision of Ipsos online polls is measured using a credibility interval. In this case, the poll is accurate to within ±2.5 percentage points, 19 times out of 20, had all Canadian adults been polled. The credibility interval will be wider among subsets of the population. All sample surveys and polls may be subject to other sources of error, including, but not limited to, coverage error and measurement error.