Over a quarter already technically insolvent, up nine points

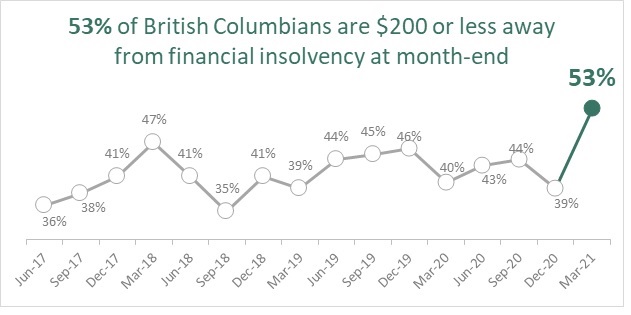

VANCOUVER, BC –April 8 , 2021 – As pandemic-related government aid and loan deferral programs begin to wind down, the latest MNP Consumer Debt Index finds the number of British Columbians hovering close to financial insolvency has reached a five-year high. More than half (53%) say they are $200 or less from not being able to pay their monthly bills and debt obligations, a whopping 14-point jump from December. This includes over a quarter (27%, +9pts) who report they are already insolvent with no money left to cover their payments at month-end.

“Financial relief measures put in place to address the pandemic provided some breathing room over the last year, but now we’re seeing a quick reversal,” says Linda Paul, a Licensed Insolvency Trustee with MNP LTD in the Lower Mainland. “The number of British Columbians with virtually no wiggle room in their household budgets has shot up significantly since December and reached a five-year high. That suggests that many are feeling anxiety about making ends meet and may start falling behind on payments or defaulting on loans, mortgages, car payments, or credit cards.”

Conducted quarterly by Ipsos and now in its sixteenth wave, the Index finds households report having less money left over at the end of the month. On average, British Columbians say they are left with $691 after making their payments, down by $161 (or 19 percent) from December — the largest drop compared to the other provinces. The decline is likely a reflection of the government aid programs, eviction bans, and debt payment relief ending.

“Some are starting to see their bills coming due, even if they’re not back to full-time employment,” says Paul. “While many are spending less and saving more, others may be sinking further into the red after job, wage, or small business loss.”

More than a quarter (27%) of British Columbians say they have taken on more debt because of the pandemic. This includes using credit cards (18%), using a line of credit (7%), taking out a bank loan (2%), or deferring mortgage payments (3%). One in five (21%) have also reported digging into emergency savings to pay monthly expenses.

“Taking on more debt just to make ends meet makes households extremely vulnerable, particularly if and when interest rates increase. The debt may become unaffordable in a higher rate environment,” explains Paul.

Half (50%) are concerned about their ability to repay debts if interest rates rise. One in three (34%) are concerned that rising interest rates could move them towards Bankruptcy.

Despite the concern, about six in 10 (63%) believe now is a good time to buy things that they otherwise couldn’t afford (+1 from December). In addition, four in 10 (43%) British Columbians say they’re more relaxed about carrying debt than usual, up five points from December and the largest increase across the provinces.

“Our findings suggest many in the province think of debt as the solution rather than the trap it can easily become,” says Paul, who urges British Columbians to be proactive about improving their financial positions and to seek professional advice concerning unmanageable consumer debt.

Yet, it seems many plan to do exactly what Paul cautions against: taking on even more credit to pay their expenses. A quarter (25%) say they plan to take on more debt to pay bills over the next year, including using high-interest options like credit cards (9%) or payday loan service (1%). The survey also found very few British Columbians plan to get professional advice (3%) or contact a Licensed Insolvency Trustee to discuss debt relief options (2%) over the next year.

“Deeply indebted individuals who find themselves taking on more debt to pay bills should seek professional debt advice right away. Licensed Insolvency Trustees offer free, unbiased advice about your individual situation and the options available,” says Paul.

Government-regulated Licensed Insolvency Trustees are empowered to help British Columbians reorganize their financial affairs and, where appropriate, can even help them avoid Bankruptcy by facilitating an agreement with their creditors. They can also guarantee legal protection from creditors through the Consumer Proposal or Bankruptcy processes.

Paul says a Licensed Insolvency Trustee may recommend one or a combination of the following depending on the extent of the debt and the individual’s overall financial situation:

Budgeting — Setting up a monthly financial plan to help balance and monitor income and expenses and potentially free up more cash to pay down debt.

Refinancing — Re-negotiating the term and interest rate on existing credit accounts to reduce the monthly cost of debts and make them easier to repay.

Liquidating — Selling high-value assets such as non-essential vehicles, recreational properties, sporting goods, and jewelry to provide the financing to pay down debt.

Consolidating — Combining all debts into a single monthly payment with a lower average interest rate to reduce the number of payments and their total cost.

Consumer Proposal — Working with a Licensed Insolvency Trustee to negotiate a legally binding debt settlement with creditors that will reduce the amount owed and can be paid over a maximum of five years. Consumer Proposals can only be administered by Licensed Insolvency Trustees.

Bankruptcy — A legal process of liquidating assets and potentially making monthly payments to eliminate outstanding debts and help insolvent consumers achieve a financial fresh start. A Bankruptcy may only be administered by a Licensed Insolvency Trustee.

“Everyone’s situation is slightly different, which is why it is important to get customized, unbiased advice from a licensed professional. Licensed Insolvency Trustees are the only debt relief professionals who can offer the full range of debt-relief options,” adds Paul.

About MNP LTD

MNP LTD, a division of the national accounting firm MNP LLP, is the largest insolvency practice in Canada. For more than 50 years, our experienced team of Licensed Insolvency Trustees and advisors have been working with individuals to help them recover from times of financial distress and regain control of their finances. With more than 230 offices from coast-to-coast, MNP helps thousands of Canadians each year who are struggling with an overwhelming amount of debt. Visit MNPdebt.ca to contact a Licensed Insolvency Trustee or use our free Do it Yourself (DIY) debt assessment tools. For regular, bite-sized insights about debt and personal finances, subscribe to the MNP 3 Minute Debt Break Podcast.

About the MNP Consumer Debt Index

The MNP Consumer Debt Index measures Canadians’ attitudes toward their consumer debt and gauges their ability to pay their bills, endure unexpected expenses, and absorb interest-rate fluctuations without approaching insolvency. Conducted by Ipsos and updated quarterly, the Index is an industry-leading barometer of financial pressure or relief among Canadians.

Now in its sixteenth wave, the Index currently stands at 96 points, up seven points compared to the last wave conducted in December 2020. Visit MNPdebt.ca/CDI to learn more.

The latest data, representing the sixteenth wave of the MNP Consumer Debt Index, was compiled by Ipsos on behalf of MNP LTD between March 4-9, 2021. For this survey, a sample of 2,001 Canadians aged 18 years and over was interviewed. Weighting was then employed to balance demographics to ensure that the sample’s composition reflects that of the adult population according to Census data and to provide results intended to approximate the sample universe. The precision of Ipsos online polls is measured using a credibility interval. In this case, the poll is accurate to within ±2.5 percentage points, 19 times out of 20, had all Canadian adults been polled. The credibility interval will be wider among subsets of the population. All sample surveys and polls may be subject to other sources of error, including, but not limited to, coverage error and measurement error.